Why personal credit score stress issues to the ILS market: Corbett, Shuriken Capital – Cyber Tech

With constructing strain and stresses in personal credit score funding markets within the headlines, the insurance-linked securities group ought to keep in mind that a carefully interlinked investor base means any fallout can have ramifications for the ILS asset class as nicely, Brad Corbett of Shuriken Capital Administration instructed us.

Corbett, the funding committee lead at lately shaped insurance-linked securities funding supervisor Shuriken Capital Administration LLC, which is backed by insurer SafePoint, is well-known for his experience throughout fastened revenue, together with private and non-private credit score.

Whereas Shuriken Capital Administration is at present centered on the disaster bond marketplace for its investments, with a plan to additionally allocate to collateralized reinsurance as nicely, Corbett’s expertise means the supervisor is conscious about how any escalation of pressures within the personal credit score area might have an effect on ILS investor sentiment and allocations.

We spoke with Corbett to seek out out extra and he defined how the Shuriken group is considering the potential ripple results for the ILS market from personal credit score being beneath strain.

Corbett defined, “Essentially the most instant dynamic is whether or not there shall be correlated redemption strain. ILS and personal credit score ETFs share the identical investor base, household workplaces, RIAs, and retail alternate options allocations. When personal credit score sells off and faces redemptions, managers rebalance throughout their whole alternate options sleeve. ILS funds can get caught in that cross-asset liquidation despite the fact that the underlying cat danger hasn’t modified in any respect. It’s pure portfolio mechanics, not fundamentals.

“The second channel is capital provide. Loads of the institutional cash that flows into ILS, significantly collateralized reinsurance and cat bonds, comes from the identical allocators who’re additionally in personal credit score. If personal credit score is marking down and triggering redemptions or capital calls, that capital is much less accessible for ILS main issuance proper now, throughout spring cat bond season. Tighter capital provide at issuance means wider spreads demanded by traders, higher entry factors for us, however more durable for cedants.

“Third, personal credit score stress is forcing a broader re-examination of illiquidity premiums. ILS, particularly collateralized reinsurance and ILWs with their 18 to 24 month capital lure, will face the identical scrutiny. Buyers who beforehand accepted ILS illiquidity at tight spreads could now demand extra compensation, which reprices the market.”

The cat bond and ILS market has all the time been uncovered to world institutional markets repricing their costs-of-capital greater and when important dangers emerge, be they from stresses in personal markets, or geopolitical threats, it can lead to strikes being taken by traders which could be more difficult to handle inside smaller asset courses.

However with personal credit score and ILS having related investor bases and typically even being in the identical funding bucket for giant allocators, the potential for stresses within the meaningfully bigger personal credit score area having ramifications for ILS are actual.

After all, when any stresses emerge in monetary markets that can be when disaster bonds and ILS shine.

Corbett mentioned, “The offsetting argument is compelling. ILS stays genuinely uncorrelated to credit score fundamentals. Cat bonds don’t default as a result of Blue Owl has liquidity points. That zero-beta-to-credit story really turns into extra engaging in a stagflationary, credit-stressed atmosphere. ILS is without doubt one of the few locations the place returns aren’t tied to financial situations. Refined allocators are beginning to acknowledge this and will rotate towards ILS as a real diversifier.

“Within the brief time period, look ahead to unfold widening on new cat bond issuances as capital provide tightens. Over the medium time period, the uncorrelated nature of ILS might make it a relative beneficiary as allocators search real diversification away from credit score. The spring issuance window would be the key take a look at.”

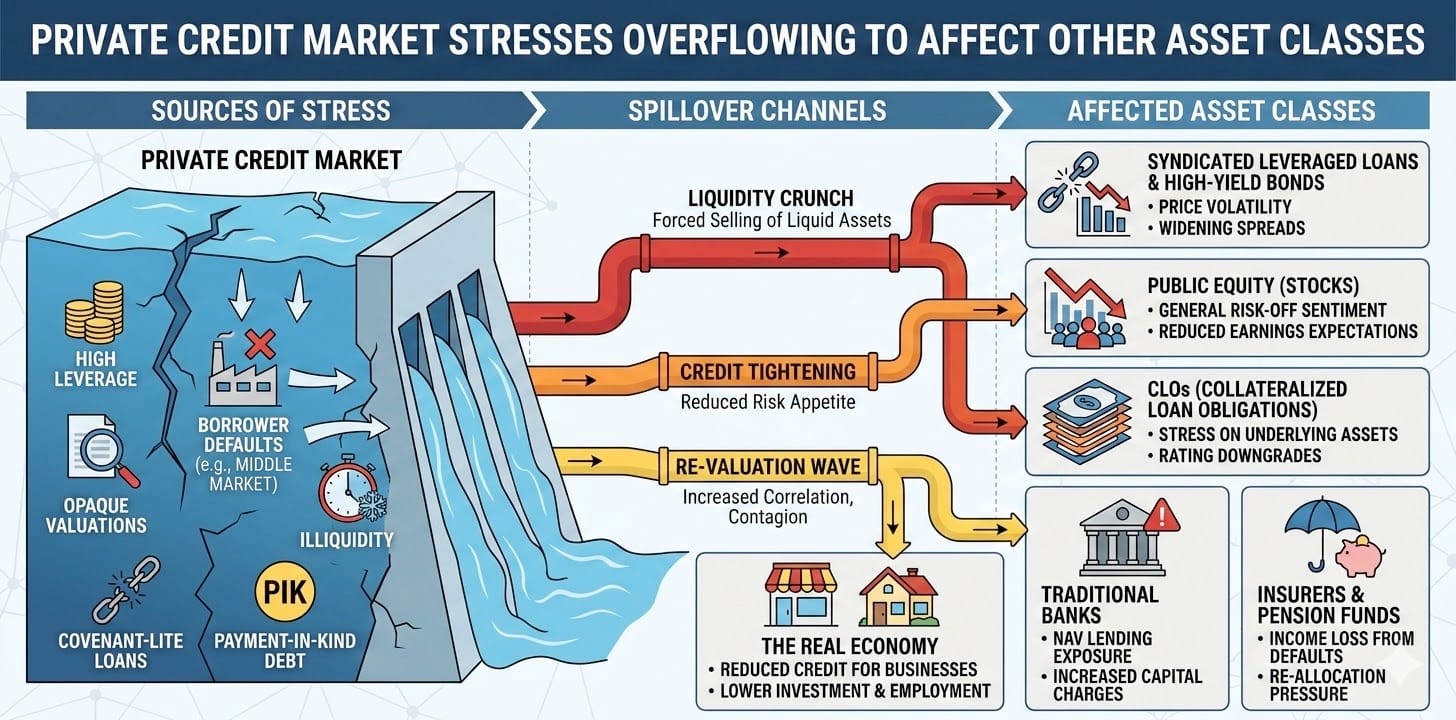

The state of affairs in personal credit score markets is complicated and could be difficult to outline. We generated an infographic utilizing AI to offer a easy overview of a few of our considering on this matter, which you’ll be able to see beneath.

Obtain the infographic right here.

Good medical health insurance ideas you’ll want to know by The Texas Insurance coverage Podcast – Cyber Tech

The best way to Journey Effectively for Seniors over 75 – Cyber Tech

Alabama Invoice Would let Alfa Federation, not Insurer, Promote Well being Plans. BCBS is Combating it. – Cyber Tech

About The Author

admin

Azeem Rajpoot, the author behind This Blog, is a passionate tech enthusiast with a keen interest in exploring and sharing insights about the rapidly evolving world of technology. With a background in Blogging, Azeem Rajpoot brings a unique perspective to the blog, offering in-depth analyses, reviews, and thought-provoking articles. Committed to making technology accessible to all, Azeem strives to deliver content that not only keeps readers informed about the latest trends but also sparks curiosity and discussions. Follow Azeem on this exciting tech journey to stay updated and inspired.