We’re just about branchless and cashless now – Cyber Tech

Thirty years in the past, I wrote a method report for NCR, the place I used to be working on the time, saying that the way forward for banking can be branchless and cashless, which was not nice information for a corporation promoting money machines.

Now, we reside in a world that’s nearing branchless and cashless. I’ve written rather a lot about department closures and the problems round that theme:

Why financial institution branches nonetheless matter (half one)

Human wants for human service (why branches matter, half two)

Branches aren’t wanted for recommendation or transactions … it’s all about belief

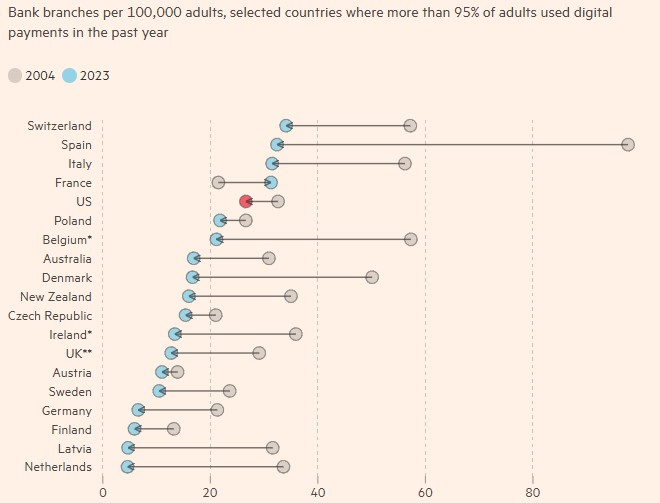

The factor is that my prediction within the Nineties was that we wanted a few tenth of the department community that we had again then. Most banks had over 1,000 branches. They solely want 100, however I by no means mentioned we might by no means want branches.

However, banks are shifting quickly away from bodily distribution and wish prospects to make use of digital providers. Over the previous decade alone within the UK, greater than 6,600 financial institution and constructing society branches have closed, a lack of greater than two-thirds of the community with closures averaging over 50 branches per 30 days.

Supply: The Monetary Occasions

Apparently, prospects don’t prefer it, as illustrated by two articles the opposite day:

Excessive-street banks ought to suppose once more about chopping in-person providers

I reside in a financial institution closure scorching spot and face paying £80 to go to my nearest department – test the listing of worst offenders

Equally, using paper in banking has been one thing we have now tried to eradicate for years. The cardboard firms Visa and MasterCard have had a struggle on money for over twenty years, and the UK Authorities determined in 2012 to ban using paper cheques for funds. Effectively, they each failed as we nonetheless use cheques and money.

The final figures I picked up are that cheque utilization has declined considerably within the final decade, however individuals nonetheless use them. Based on stats from UK Finance, Brits banked 91 million cheques in 2024. The identical with money. Utilization has declined, however we nonetheless like money.

LINK, which runs the UK’s ATM community, ran a survey of 1,116 excessive avenue SMEs in September 2025 to evaluate money acceptance and cost habits, and located that money is perhaps not King but it surely’s nonetheless related.

You may obtain the report right here however right here’s a fast abstract:

Money is declining however nonetheless broadly used

Money use within the UK is falling quickly as shoppers more and more use playing cards, telephones, and digital funds. Money now represents lower than 10% of whole funds, and ATM withdrawals on the LINK community have fallen considerably since 2018.

Nonetheless, money stays essential for many individuals—particularly those that are financially weak, digitally excluded, or utilizing money for budgeting.

Most high-street companies nonetheless settle for money

The survey of 1,116 UK SMEs discovered that:

- 77% of high-street companies nonetheless settle for money

- 46% of in-person transactions are money

- 55% of companies actively encourage money funds

- 14% of shops went cashless previously 12 months

Money acceptance varies by location:

- City areas: ~80% settle for money

- Suburban/coastal areas: ~72% settle for money

Why companies are going cashless

Retailers aren’t abandoning money purely due to falling demand. The primary drivers are operational pressures:

High causes companies cease accepting money

- Fraud dangers (counterfeit notes)

- Safety considerations and theft threat

- Declining buyer demand

- Money-handling prices (deposit charges, insurance coverage, transport)

- Simpler bookkeeping with digital funds

Financial institution department closures and restricted deposit services additionally make dealing with money more durable for companies.

Money nonetheless presents actual benefits

Regardless of the shift to digital funds, money continues to offer essential advantages for retailers and shoppers:

- Avoids card processing charges

- Instant liquidity for small companies

- Quicker small transactions

- Works throughout web or system outages

- Helps financially weak prospects

For these causes, many retailers imagine money helps inclusion and resilience on the excessive avenue.

Money acceptance is anticipated to maintain falling

The analysis suggests the decline will proceed:

- 56% of shops say money utilization has fallen previously two years

- 55% anticipate additional decline

- 4% plan to cease accepting money inside two years

Greater than half of companies (51%) imagine declining money acceptance harms the excessive avenue, lowering accessibility and buyer inclusion.

Key dangers recognized

The report warns that with out intervention the UK may develop a “two-tier cost society”, the place individuals who can not use digital funds wrestle to take part in on a regular basis commerce.

This is able to have an effect on teams comparable to:

- Low-income households

- Aged individuals

- Digitally excluded people

- Victims of economic management or abuse

Suggestions from the report

To protect cost selection, the report recommends:

- Strengthen money deposit infrastructure (banking hubs, Submit Places of work, deposit ATMs).

- Deal with retail crime and fraud to scale back safety dangers linked to money dealing with.

- Monitor money acceptance (not simply entry to money withdrawals).

- Promote a balanced funds ecosystem the place each digital funds and money coexist.

The underside line is that money is declining however stays economically and socially essential. Whereas most companies nonetheless settle for it, rising prices, safety dangers, and shrinking banking infrastructure are pushing retailers towards cashless fashions. So sure, we at the moment are turning into branchless and cashless whether or not we prefer it or not.

Postnote: whole apart however the UK is ending its analogue phone system from January 1 2027. It is digital solely.

Are Listed Common Life Insurance coverage Insurance policies a Good Possibility or a Rip-off? – Cyber Tech

Outdoors In | AI backlash is rising, however how a lot is simply hype? – Cyber Tech

Zacks Small Cap Analysis – BBLG Financials Present Firm in Strong Form – Cyber Tech

About The Author

admin

Azeem Rajpoot, the author behind This Blog, is a passionate tech enthusiast with a keen interest in exploring and sharing insights about the rapidly evolving world of technology. With a background in Blogging, Azeem Rajpoot brings a unique perspective to the blog, offering in-depth analyses, reviews, and thought-provoking articles. Committed to making technology accessible to all, Azeem strives to deliver content that not only keeps readers informed about the latest trends but also sparks curiosity and discussions. Follow Azeem on this exciting tech journey to stay updated and inspired.