Life replace #3 – Enterprise as normal? – Whole Steadiness – Cyber Tech

Hola compadres!

(We’ve simply bought again from a weeks trip in Spain, so naturally I’m now fluent in Spanish!…Not).

We’re approaching this blogs sixth birthday, so I assumed I’d higher offer you guys an replace on the venture and the life within the Whole Steadiness family.

The summer season glided by simply as shortly as spring got here and went 🙁 Summer season is my favourite time of the 12 months right here in Denmark, and we’re now slowly making ready ourselves for an additional lengthy winter (such is the lifetime of us northerners).

When individuals ask me

“So, are you accomplished with the home venture but?”

I inform them that I really feel we’re 95% there, however in actuality once you stay in an older home, you’re by no means actually going to succeed in 100%…There’s all the time going to be one thing that wants fixing (or the spouse begins new tasks!). However by way of the renovation of the within of the home, we really feel that we’re 95% there. We’re nonetheless lacking some trim and a few of our closets nonetheless don’t have doorways! (We will’t agree on which doorways to get, and in addition we actually don’t need to spend extra money on closets! haha).

Then there’s the surface of the home. Outdoors “renovations” is (if you happen to ask me) a summer season job, so the window of alternative has form of already handed us by. Naturally, my spouse don’t share that opinion (as you possibly can think about)…

As a result of we nonetheless have some exterior “renovations” to complete, we’ve bought some constructing provides saved exterior, so it’s nonetheless wanting considerably like a constructed website. It might be good to get these tasks completed (however they price money and time!), so we might additionally benefit from the exterior of the home/backyard.

Anyway, we nonetheless have tasks to complete earlier than we are able to say that we’re DONE. So we’ve not gotten the home appraised but, so we nonetheless don’t know if the financial institution worth the renovation as a lot as we do. I do know you guys love the numbers, so I’ve accomplished a fast tally of the foremost objects.

Right here is the finances for the renovation, in comparison with the precise spend (a few of them are estimates):

As you possibly can inform, we managed to blow previous our finances in virtually all main classes…

And sadly, this sheet doesn’t cowl all our precise spending. We’ve spent roughly DKK 100-150.000 greater than this on: I’ve no fucking clue 🙁

All of the “small stuff” provides up. I get in a foul temper simply by serious about this, however I don’t need to paint the image brighter than it truly is. Be VERY cautious if you happen to take into account endeavor a renovation of this magnitude your self…I can’t actually advocate it, until you’ve very deep pockets! 😛

If we set a conservative worth on our present dwelling – now after the renovation – we’re simply breaking even. If we advertise right this moment at what I imagine can be an optimistic worth, our efforts would web us a yield of roughly 10%. Since this could be tax free, I suppose it’s not a foul yield for 8 months work, however had you instructed me that this could be the end result previous to the reno, I’d positively have stated “no thanks”.

However not the whole lot may be measured in financial worth 🙂 The transfer to a brand new location has given us and our daughter a complete new stage of freedom and pleasure. Our daughter walks to and from college day-after-day, and this has freed up greater than 1 hour of our time day-after-day (commuting to and from college). She will be able to additionally now stroll to most of her mates, and this has given her a complete new feeling of independence. It has been all price it after we see how far more pleasure she will get from being nearer to her mates. SHE nonetheless doesn’t acknowledge this truth but – she nonetheless typically say we must always have stayed within the previous home, as a result of then we might have averted all of the stress and exhausting work of the reno. I believe in time, she may even be capable to see that it was all price it 🙂

The transfer was additionally about reducing our “working prices”, and this may even positively profit us going ahead.

Now that the curiosity has begun to say no a bit (for now), subsequent 12 months ought to see respectable financial savings in our month-to-month finances as we presently have a 1-year flex-mortgage. Which means that on January 1st 2025 our mortgage will get a brand new rate of interest.

We presently pay 4.05% (+ charges) and the brand new price is presently hovering round 3% for the 1-year flex mortgage. Nonetheless, if you happen to repair the speed for five years you possibly can safe a price round 2.65% (+ charges). The charges differ relying in your LTV, but additionally relying on how lengthy you repair it for. For some motive our financial institution favor the 1-year over the 3- and 5-year fastened mortgages. We presently pay 0.57% in price (bidrag) to the financial institution on-top of the 4% rate of interest. If we convert to 3-year fastened price we then must pay 0,77% in price!? This is senseless to me, as this has LESS danger than the 1-year fastened. If we repair it for five years the price is 0.65%. Which means that proper now, the most affordable (and most secure possibility) can be to repair the speed for five years, which might give us a mixed price of three.3% (curiosity+price). From a historic perspective that may be a pretty whole lot…

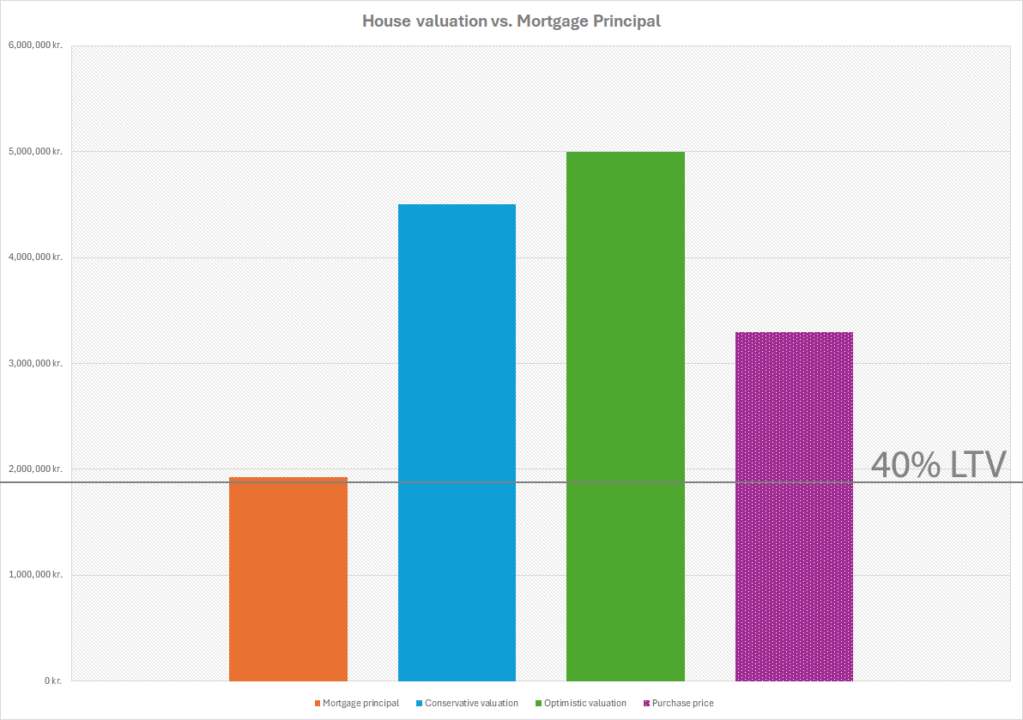

Nonetheless, our present mortgage is granted primarily based on a 60% LTV. If we get a good valuation, we might presumably hit <40% LTV. Why does this matter? This could put us in a decrease fee-bracket (however it’ll require us to pay the financial institution to problem a brand new mortgage, which additionally has a price).

If we take the common of the conservative valuation (estimated) and the optimistic valuation (estimated) we’re simply 10 month-to-month funds from reaching 40% LTV.

For some motive, the <40% mark is the holy grail. It’s a ladder that goes from 80% to 60% to 40%. In the event you’re beneath 40% LTV the financial institution is contemplating you “low danger”. They thus reward you with a reduction on the price (bidrag). In our case, if we get a valuation someplace between what we take into account because the conservative (4.5 million) and the optimistic (5.0 million) we’re throughout the 40% LTV vary. However we’re presently on a 30-year mortgage (with 28.5 years left), and getting a brand new mortgage is just not free. Sadly this ladder doesn’t routinely work in your favor in your present mortgage. That is clearly a “bank-trick” that requires you to PAY for a brand new mortgage with a view to drop right into a decrease price bracket. Typical dipshit bank-move. Anyway, the price financial savings solely quantities to 0.20% in our case (going from the 60% LTV bracket to the 40% LTV bracket), so it’s extra a matter of principal for me than one thing that really characterize an ideal financial worth. 0.20% in financial savings over the subsequent 10 years does nonetheless quantity to greater than €4.000 – however getting a brand new mortgage might simply run us €1.500…That leaves €2.500 in potential financial savings.

For now my conclusion on this matter is that it doesn’t make sense for us to PAY to get a brand new mortgage, until the brand new mortgage offers us one thing that our present mortgage doesn’t.

ENTER: The choice of getting a 10-year fastened 3% mortgage (right here the price would solely be 0.30%). This could imply that we’d be debt free in 10 years. It might additionally save us a ton in curiosity funds (if we repay our mortgage in 10 years as an alternative of 30). In fact it might see our month-to-month mortgage funds double in comparison with right this moment…This could imply that we’d not have a lot left to place in direction of our Whole Steadiness. The whole lot can be used to pay down the mortgage…

What do you guys assume? What would you do?! 🙂

Since we’re nonetheless in a “rebuild”-phase each by way of our money reserves and our precise dwelling, I really feel like we’re nonetheless residing inside a venture.

Sadly my psychological state has additionally been considerably deteriorating as of late. It’s been a very long time (years) since I keep in mind feeling “on prime”. I believe it’s time for me to conclude and simply put it on the market “on paper” that I’m affected by a gentle despair. I really feel like I’ve misplaced the power to really feel enthusiastic about something. I don’t have any hobbies, and I’ve develop into a grumpy previous man. A buzz kill. This in all probability began approach again (earlier than I even began this weblog) and it’s been like being on a curler coaster these previous few years. Few highs, many lows. We might additionally simply name it a mid-life disaster, however on condition that this began in my early 30’s I believe that might be a bit unfair. I’ve been looking for other ways to “elevate my spirits” and lift my temper, however I’ve but to seek out the silver bullet.

I’m presently sad at work, and that shortly spills over into my dwelling life, which is actually unfair to my household. I’ve realized that I actually can’t save myself to happiness, however having 0 cash in my account positively doesn’t elevate my spirit both! I’m hoping that after our spending normalizes and our financial savings as soon as once more start to develop, I’d really feel a momentary elevate in spirit – however I do know that it is going to be brief lived. I’ve bought to discover a extra everlasting repair to my curler coaster. I hoped that somebody smarter than me had the reply, however he too disillusioned. Happiness comes from inside, however spending an excessive amount of time in your individual head appears to have the alternative impact (at the very least that’s my expertise).

Don’t fear, I’m not suicidal or something, however I simply can’t appear to seek out contentment in attempting to outlive day-after-day. It doesn’t look like a lot of a life, if you happen to can’t discover enjoyment in even the little issues. It’s in all probability time to go to a(nother) therapist 🙂

Yesterday the spouse and I attempted cryotherapy. 3 minutes in a cryo-chamber in your underwear was a fairly wild expertise! Earlier than that we had spent half-hour in a sauna, so it was an enormous distinction. Warmth is just not my factor, however the chilly shock I really feel like would possibly maintain some potential. 3 minutes of you simply attempting to breathe and block out the acute chilly. Survive for 3 minutes and fear about the remainder later.

The spouse has bought an ice-bath now… Want me luck! HAHA

Till subsequent time!

Zacks Small Cap Analysis – SYRA: Takeaways from Life Science Investor Discussion board Presentation – Cyber Tech

– Cyber Tech")

Apple Inventory: Imaginative and prescient Professional May Be A Main Risk To Profitability (NASDAQ:AAPL) – Cyber Tech

Zacks Small Cap Analysis – SVRE: OEM settlement with IVECO introduced and the corporate introduces a brand new SaaS income mannequin. Dilution danger stays a priority. – Cyber Tech

About The Author

admin

Azeem Rajpoot, the author behind This Blog, is a passionate tech enthusiast with a keen interest in exploring and sharing insights about the rapidly evolving world of technology. With a background in Blogging, Azeem Rajpoot brings a unique perspective to the blog, offering in-depth analyses, reviews, and thought-provoking articles. Committed to making technology accessible to all, Azeem strives to deliver content that not only keeps readers informed about the latest trends but also sparks curiosity and discussions. Follow Azeem on this exciting tech journey to stay updated and inspired.