Apple: Points Are Overblown However Outlook Is Unsure (NASDAQ:AAPL) – Cyber Tech

ozgurdonmaz

I do not get the bears. However I do not get the bulls both. Apple Inc. (NASDAQ:AAPL) is a big enterprise and as such it should take pleasure in plenty of consideration. Consequently, an enormous downside that shareholders and potential traders face is noise. Tons and many noise.

This text is my try to chop by that and supply a extra sober view of Apple’s most up-to-date outcomes, how they evaluate to the earlier interval, in addition to present that each present points and prospects do not carry sufficient weight to justify both a bearish or bullish thesis in the intervening time.

You could be glad to know that I haven’t got pores and skin within the recreation due to the present worth. Then once more, you might not. However it’s laborious to disclaim that this could possibly be of worth to many traders who want a break from echo chambers.

Let’s get began…

The Efficiency Hasn’t Been Spectacular, However It is Not Dangerous Both

To get an thought of the place the enterprise may be heading, let’s first begin with the latest outcomes that the corporate launched for its December quarter final yr. Needless to say the quarter had one much less week than the December quarter of 2022.

To begin with, its income reached $119.6 billion which mirrored a modest enhance of two% on a YoY foundation. It is vital to notice, nonetheless, that the earlier quarter had the advantage of an extra week and that the iPhone provide was constrained due to manufacturing facility shutdowns resulting from COVID, each of which contributed to a 200 bps headwind in accordance with administration. On the similar time, Apple appears to be having fun with all-time income data in Europe and double-digit progress in most rising markets.

Let’s now break down income for a minute. At $69.7 billion, iPhone gross sales elevated by 6% within the final reported quarter because the similar quarter the yr earlier than. As a reminder, the phase represents the vast majority of income (58.32%). Mac gross sales had a extra modest enhance of 1% YoY, reaching $7.8 billion and represented 6.52% of complete income.

As for iPad, gross sales have been 25% decrease YoY, at $7 billion; we should always notice that in the course of the earlier quarter, Apple launched the iPad Professional and iPad 10 technology which contributed to a naturally tough comparability. To not point out the additional week of gross sales on high of that issue. iPad gross sales represented 5.85% of complete income.

One other disappointment could have been the 11% YoY lower in Wearables, Residence, and Equipment income which got here in at $12 billion (10% of complete gross sales). Consider, although, that the December quarter in 2022 loved the profit introduced by the launching of AirPods Professional 2nd technology, the Watch SE, and the primary Watch Extremely, plus the additional week of gross sales.

Final, the Companies phase skilled an all-time gross sales report of $23.1 billion which mirrored a YoY enhance of 11%. That is vital because the phase represents a big contributor to income at practically 20% of complete gross sales for the quarter.

Now, the gross margin was 45.9% for the corporate, a 70 bps linked-quarter enhance. Zooming in, the margin for the merchandise phase was 39.4%, a 280 bps linked-quarter progress, and the margin for providers was 72.8%, a 190 bps enhance.

Furthermore, internet earnings elevated by $3.9 billion to $33.9 billion on a YoY foundation and diluted EPS got here in at $2.18, reflecting a 16% YoY progress in addition to an all-time report. Final, money circulation from operations was at $39.9 billion, rising by 17.3% YoY.

Trying ahead, administration has offered some steering that’s based mostly on at the very least steady macroeconomic situations. Shareholders can count on the March quarter to be flat in comparison with the identical quarter in 2023 by way of complete and iPhone gross sales. Nevertheless, administration expects Companies income to mirror an identical double-digit progress on a YoY foundation as within the earlier quarter. Final, some modest to reasonable enlargement is forecast for the gross margin at 46-47% (up from 45.9% within the final reported quarter).

As you may see, the efficiency was roughly flat, however some acceleration in progress was skilled in sure segments, probably offset by decrease profitability in others. Though justification for a few of these outcomes is out there, traders ought to remember that there isn’t a clear indication of short-term progress. On the similar time, I imagine that there’s nothing that ought to trigger panic for shareholders.

Points Are Overblown

What concerning the long-term headwinds although? Shareholders ought to maintain an in depth eye on the present occasions that might have a big impression on Apple’s backside line. And traders ought to perceive how these occasions contribute to the general threat profile of the inventory.

However as at all times, the bears are going to magnify every part that is occurring with giant firms to verify their bias. And this time is not any completely different.

Take China gross sales, for instance. The lower in the course of the December quarter was 13% on a YoY foundation in that market and but the corporate managed to compensate and beat iPhone revenues. Certain, 17.41% of complete income got here from China. Nevertheless, is a latest shrinkage in gross sales of that magnitude a motive for shareholders to dump their shares and traders to quick the inventory? At most, it’s a trigger for concern and the necessity for shut monitoring for shareholders; the rest seems to be fear-mongering.

One other promoting level for bears is the compliance of Apple with the European Union’s Digital Markets Act, which includes the allowance of iPhone apps to be downloaded from builders’ web sites. Does this open the door for a revenue margin compression provided that Apple can cost builders as a lot as 30%? Certain. Can that considerably have an effect on the corporate’s backside line? That is unsure, however there’s a good likelihood that it will not.

First, Apple has been clear that it will not be capable of present prospects the identical stage of safety if they do not go for its app retailer, to not point out the resolutions of different points equivalent to refunds. So, shareholders ought to remember that it is as much as how the market behaves; the worth proposition supplied by Apple could also be so a lot better that prospects will not change their habits.

Second, the EU app retailer market represents a small portion of the worldwide one by way of income, so it is unlikely that the regulation will trigger something greater than a really small dent even when prospects do change their habits consequently. Within the CFO’s personal phrases:

Simply to maintain it in context, the modifications utilized to the EU market, which represents roughly 7% of our world app retailer income.

Final however not least, there may be additionally the antitrust lawsuit that was filed by the DOJ in opposition to Apple on March 23, for which the idea is the alleged violation of antitrust legal guidelines. As an example, the lawsuit argues that Apple has prevented different firms from offering providers by apps that may compete with Apple’s personal apps. It additionally argues that it is laborious for iPhones to be related with smartwatches that are not Apple Watches. One other instance is that Apple would not enable builders to make use of the iPhone’s NFC with their very own digital wallets as a result of they’d compete with the Apple Pockets.

Based mostly on the New York Instances, authorized specialists have famous that it’s authorized for firms to favor their very own choices. Due to this fact, the federal government want to have the ability to articulate why it is a completely different case with Apple.

A extra particular potential weak spot within the lawsuit is revealed by the truth that it has to resort to drawing parallels between this case and the one the place Microsoft (MSFT) was limiting the usage of different internet browsers twenty years in the past. Quoting from the grievance:

In 1998, Apple co-founder Steve Jobs criticized Microsoft’s monopoly and ‘soiled ways’ in working methods to focus on Apple, which prompted the corporate ‘to go to the Division of Justice’ in hopes of getting Microsoft ‘to play honest,.

Although the court docket discovered the corporate in violation of Part 2 of the Sherman Act, now could be completely different. To begin with, a Supreme Courtroom ruling that got here after that case acknowledged that companies can’t be sued for merely not aiding opponents to compete in opposition to their services or products. If the DOJ fails to argue that Apple does something greater than merely not making it straightforward for opponents to seize market share, then Apple attorneys could not must work very laborious.

One other factor we should always notice is that again then, Microsoft had a ~95% share of the OS marketplace for Intel PCs, whereas the DOJ claims that Apple has about 70% on this case. It appears to me that it will be very laborious to show a monopoly right here.

Let’s not additionally overlook that within the Epic Video games v. Apple case, the choose dominated in favor of Apple after the latter efficiently made a case for the safety it’s higher in a position to present by stopping Epic Video games from distributing its recreation exterior Apple’s app retailer. It’s nearly sure to me, at the very least, that it’ll defend its practices by interesting to safety considerations right here as properly.

Final, until the DOJ has some proof we’re unaware of, there may be additionally a weak spot relating to the alleged monopoly that Apple is allegedly sustaining unlawfully as a result of the DOJ implies that the corporate obtained its monopoly lawfully. As Lloyd Constantine, an legal professional, informed Funds Dive:

In the event that they received their monopoly lawfully, which … is tacitly admitted on this grievance, then, in what methods did they start to keep up that monopoly unlawfully?

It seems that the DOJ could have its arms full for the subsequent few years. For now, Apple has acknowledged that it will file a movement to dismiss, in all probability throughout the subsequent couple of weeks.

The Different Supply of Noise

Regardless, the bulls are speculating as properly. What we might be fairly assured about is that Apple is dedicated to driving shareholder worth by share repurchases. As an example, the corporate purchased again $76.6 billion value of frequent inventory in the course of the fiscal yr 2023. Within the December quarter, it purchased 118 million shares for $20.5 billion. These items are quantifiable.

Concerning Apple’s investments in AI expertise, nonetheless, issues usually are not as sure but. There’s speak that Imaginative and prescient Professional goes to outperform each Meta Quest 2 and Sony VR in gross sales in the long run. There are additionally rumors surrounding the preorder gross sales numbers. In any case, these can solely serve speculators and are of little worth to shareholders and traders.

Administration would not assist a lot right here both as a result of it is vitally secretive about its plans; all they are going to share in the intervening time is how excited they’re to be working in that space, however this may not minimize it. Whereas there may be a superb motive for that, the actual fact stays we do not have entry to stable information but.

There isn’t any denying on my half that Apple could have a superb alternative to seize important AI expertise market share sooner or later. However basing my funding selections on this cheap but imprecise assertion could be a foul thought; even when issues work out alright. I believe it is higher to attend for the corporate to announce extra monetary information relating to Imaginative and prescient Professional earlier than we even begin enthusiastic about the long-term impression the product could have on its backside line.

The Challenge of Worth

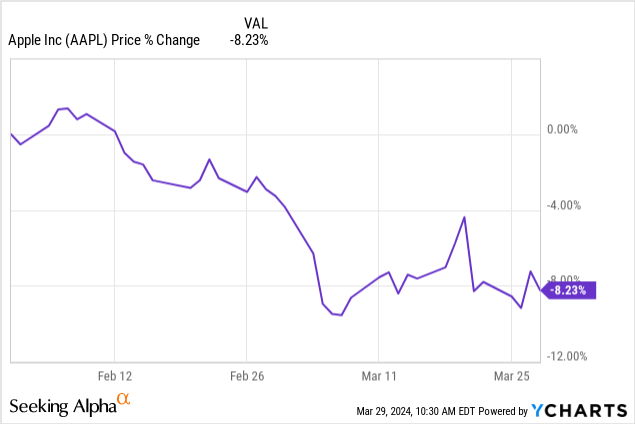

The opposite downside with being bullish is the present worth. It is true that the autumn was important for AAPL not too long ago:

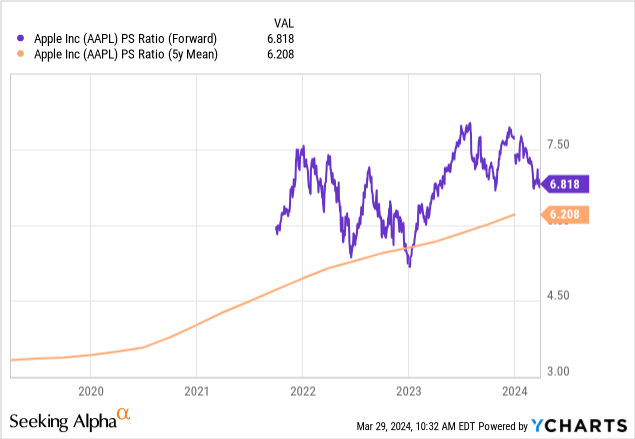

Maybe the market is changing into extra conservative with the inventory. Nevertheless, the worth hasn’t skilled a lot strain within the final couple of years. It’s nonetheless overvalued based mostly on a couple of metrics. As an example, its income a number of is above its 5-year imply:

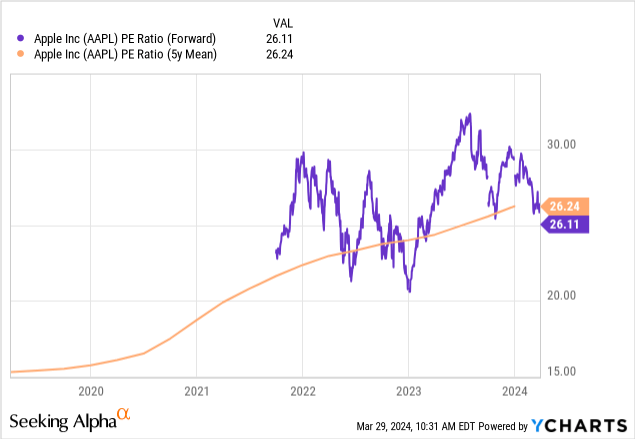

And the identical goes for the earnings a number of, which is sort of the identical because the 5y imply:

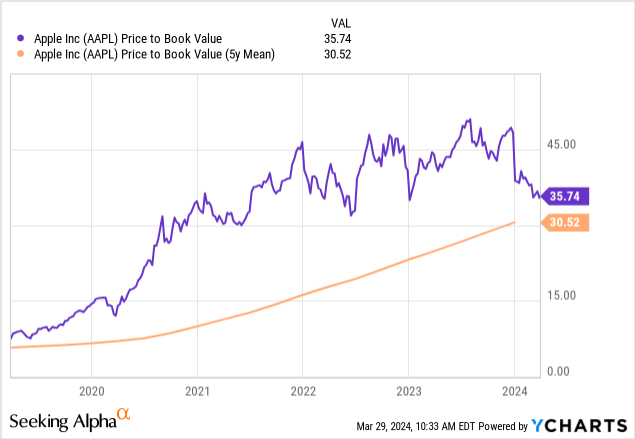

Final, its P/B ratio shouldn’t be solely above the 5-year imply, however is exceptionally excessive in the intervening time:

A legitimate argument could possibly be made in opposition to utilizing the previous as one thing related on the idea that it would not signify the state of the enterprise sooner or later. And I might respect that. However I additionally view the justification of shopping for AAPL at any worth due to potential future enterprise developments as primarily speculative and unfit to serve traders properly of their decision-making. Within the absence of a greater approach to gauge worth attractiveness, I believe the short-term previous is all we now have. We could miss a possibility, however we at the very least will not be shopping for a enterprise that’s valued based mostly on what might occur as a substitute of what has already occurred and what’s.

On the finish of the day, what’s will at all times be higher to base funding selections on than what’s going to be. Typically, speak of undervaluation springs from discounted money circulation, or DCF, fashions. The difficulty shouldn’t be at all times the assumptions that analysts make, however the magnitude of these assumptions to reach at an “outperform” worth goal. I’ve no downside in any respect with them serving speculative operations. However a line have to be drawn between these and investing.

A Few Dangers

By now, you in all probability already perceive a number of the dangers of investing in AAPL, however let’s briefly point out them.

First, it wasn’t my intention to downplay the gross sales decline in China over the past reported quarter. I simply suppose it is unsound to make use of this truth to trigger panic. That being stated, this does signify a threat as a result of if a development types it might have a major impression on profitability due to how huge the reliance is on China. Due to this fact, I believe that shareholders ought to monitor this from quarter to quarter.

One other threat is expounded to the DOJ lawsuit. Although it would not seem to have benefit in my view based mostly on the data we now have, Apple could must pay a high quality. One bullish analyst talked about the potential of a “hefty high quality” and stated that because the case will not be resolved any time quickly, there may be additionally a headline threat.

Final however not least, the present worth stage additionally creates a threat. Whereas I do not suppose that any promoting strain can stick with AAPL for very lengthy, traders might want to pay attention to a possible alternative price they may incur.

The Verdict

So, the place are we? Based mostly on what we now have stated up to now, long-term Apple Inc. shareholders may be immune to promoting shares and the present noise made by the bears should not make such resistance unreasonable. Those that do not but have a place in Apple Inc. like me may be higher served to remain on the sidelines for now as a result of there may be additionally plenty of noise involving prospects with out concrete information that ignores the present worth of AAPL.

For these causes, I’m score the inventory a maintain for now and I will eagerly await the subsequent quarterly report and earnings name.

Earlier than you go, I’ve some questions for you:

- What’s your opinion on gross sales lowering in China? Do you suppose it signifies rising competitors that’s prone to persist?

- Do you suppose Apple should pay a “hefty” high quality in regard to the DOJ lawsuit?

- How do you view the gross sales potential of the Imaginative and prescient Professional? Do you suppose it should have a major impression on Apple’s backside line sooner or later?

I need to thanks for studying and, please, when you preferred this text, let me know within the feedback. It means loads to me.

The Editors: BBC World Information strikes to Broadcasting Home – Cyber Tech

(NASDAQ:AAPL) – Cyber Tech")

United States V. Apple: The Winner Might Be You (Score Improve) (NASDAQ:AAPL) – Cyber Tech

Enabling Self-Indulgent Grownup Youngsters Is Not Good Parenting – Cyber Tech

About The Author

admin

Azeem Rajpoot, the author behind This Blog, is a passionate tech enthusiast with a keen interest in exploring and sharing insights about the rapidly evolving world of technology. With a background in Blogging, Azeem Rajpoot brings a unique perspective to the blog, offering in-depth analyses, reviews, and thought-provoking articles. Committed to making technology accessible to all, Azeem strives to deliver content that not only keeps readers informed about the latest trends but also sparks curiosity and discussions. Follow Azeem on this exciting tech journey to stay updated and inspired.