Apple Inventory: Imaginative and prescient Professional May Be A Main Risk To Profitability (NASDAQ:AAPL) – Cyber Tech

Nikada/iStock Unreleased through Getty Photographs

Apple’s (NASDAQ:AAPL) administration has introduced that they are going to be launching Imaginative and prescient Professional in China this 12 months. The corporate is going through vital challenges in China and has reported a significant dip in income in this area. Whereas a variety of media consideration has been given to Imaginative and prescient Professional, it’s unlikely that this system will transfer the needle by way of income within the close to time period. However, large R&D funding is required to construct this system which is already affecting the margins of the corporate. CNBC reported the invoice of supplies of Imaginative and prescient Professional is the same as $1,542 making it troublesome for Apple to offer value cuts. Apple is already going through margin headwinds because of different low-margin companies like TV+ as talked about within the earlier article. If the investments in Imaginative and prescient Professional attain a stage much like its competitor Meta’s (META) Actuality Labs, we might see a major decline in Apple’s profitability within the subsequent few quarters.

We have to have a look at a few of the services of Apple which haven’t carried out properly when they’re in direct competitors with different home Large Tech corporations. This may give a sign of the problem confronted by Apple’s Imaginative and prescient Professional in its competitors with Meta. Apple has not carried out properly within the sensible speaker phase the place it’s in direct competitors with Amazon (AMZN) and Google (GOOG). Apple’s sensible audio system haven’t been in a position to achieve a significant market share regardless of one of the best efforts of the corporate. Apple has additionally not been in a position to present good subscriber development in its video streaming TV+ phase. Google’s YouTube Music has not too long ago introduced reaching 100 million subscribers which has possible overtaken Apple Music regardless of Apple having a giant head begin.

Meta has reported losses of $42 billion in Actuality Labs phase since 2020 when it began reporting the information. If Apple must compete with Meta, it might possible be investing the same quantity on this phase which might negatively have an effect on the underside line by greater than 15%. Webdush analyst Dan Ives has estimated that Apple will promote 1 million models of Imaginative and prescient Professional in 2025. This is able to equate to an extra $3.5 billion in income contribution for Apple. The income contribution of Imaginative and prescient Professional in 2025 could be lower than 1% of the general income and fewer than 10% of the Wearables phase the place Apple is reporting double-digit YoY decline in income. Imaginative and prescient Professional phase can turn into an enormous cash pit if the adoption price doesn’t enhance dramatically. Whereas a variety of consideration is given to Imaginative and prescient Professional, Apple’s core enterprise can be going through headwinds because of antitrust points, falling income, and challenges in China.

Points with pricing

Essentially the most talked about side of Imaginative and prescient Professional is its value. At $3,499, it’s out of the vary of most clients. Apple might have selected this value with the intention to sign the premium high quality of the system. Nevertheless, the invoice of supplies of Imaginative and prescient Professional can be fairly excessive. Third-party estimates have urged that the invoice of supplies is $1,542 per set which is larger than the retail value of Quest Professional. The shows of Imaginative and prescient Professional have been praised so much, together with by Mark Zuckerberg, nonetheless they price $228 for every eye. It’s extremely possible that Apple will launch a lower-priced model of this system within the subsequent few quarters. However even at a cheaper price level, it might price a bit for purchasers.

Firm Filings

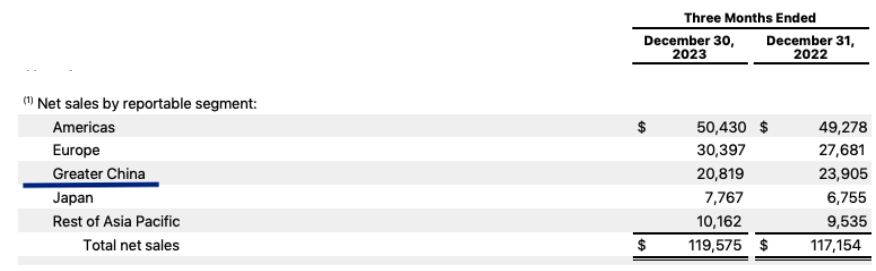

Determine: Decline in Apple’s gross sales in China. Supply: Firm Filings

Apple’s administration has not too long ago introduced that they are going to launch Imaginative and prescient Professional in China this 12 months. This could assist the declining gross sales numbers on this vital area. Nevertheless, Chinese language clients have not too long ago been pulling again from making luxurious purchases because the economic system continues to really feel new headwinds. Even luxurious model Gucci has introduced a giant decline in its enterprise in China which is usually a warning signal for Apple.

I consider that mass adoption of those units won’t begin at a value above $1,500 and Apple might want to minimize on many vital options of Imaginative and prescient Professional to achieve this value vary.

Apple’s competitors with Large Tech

Apple’s earlier report in competing head-on with different Large Tech corporations has been combined. I consider, one of many greatest latest failures for Apple has been its incapability to extend the market share of sensible audio system. Each Amazon and Google have been in a position to retain their market share within the sensible speaker and sensible dwelling units phase regardless of value cuts supplied with Apple’s HomePod. Even a lower-priced HomePod Mini didn’t change the market share so much for Apple.

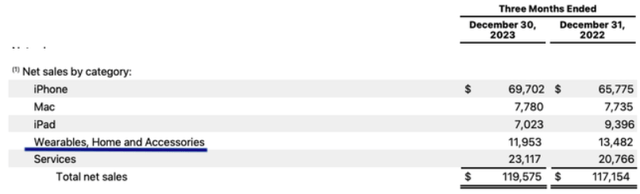

Firm Filings

Determine: Apple reported double-digit decline in Wearables in latest earnings. Supply: Firm Filings

Apple’s Wearables has declined by double-digit within the latest earnings on the again of one other 8% decline within the year-ago quarter. Previous to the pandemic, in Q1 2020, Apple introduced $10 billion income within the Wearables phase. During the last 4 years, the CAGR development on this phase has been lower than 5%. At one level, Apple’s administration touted the Wearables as the subsequent main income driver throughout the Merchandise class for the corporate. It now hopes that Imaginative and prescient Professional would be the subsequent large factor for the corporate however Imaginative and prescient Professional faces a giant problem from Meta.

Meta has gone all-in with its Actuality Labs. It has invested tens of billions of {dollars} on this phase and has had a giant head begin. Quest collection has cumulatively shipped over 20 million models and Apple will discover it troublesome to get near this quantity within the close to time period. It’s unlikely that Meta will quit its market share simply. If Apple’s market share on this phase stays in single-digit or low double-digit, it might enhance the bearish sentiment in the direction of the inventory.

Largest cash pit in historical past

The R&D expense behind this system shouldn’t be underestimated. Meta has reported $42 billion in cumulative losses since 2020 in Actuality Labs. This reveals the staggering stage of analysis effort required to construct the system and its ecosystem. Apple would possible be investing the same quantity to construct its personal ecosystem. Apple doesn’t break down the expense however Tim Cook dinner talked about concerning the scale of investments throughout the launch of the product.

There’s 5,000 patents within the product, and it’s constructed on many inventions that Apple has spent a number of years on from silicon to shows and vital AI and machine studying.

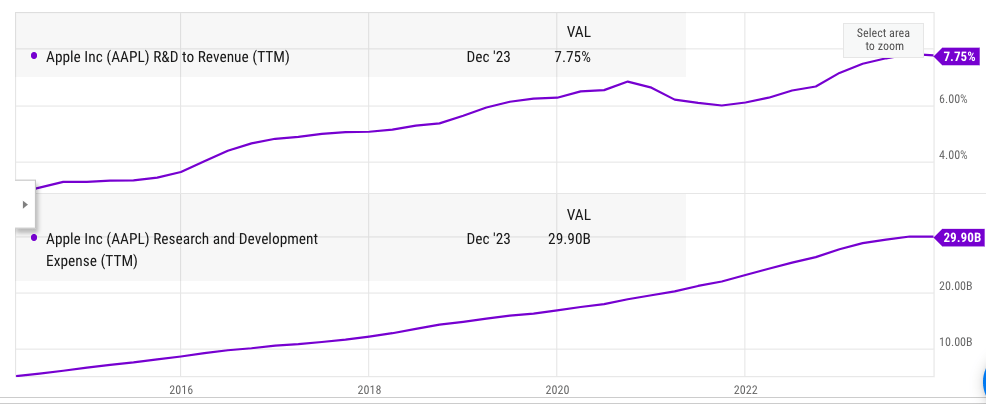

Traders may also gauge the bills by the huge enhance in R&D invoice over the previous few years. The ttm R&D expense for Apple has elevated from lower than $5 billion in 2014 to $30 billion within the latest quarter. This has additionally elevated the R&D to income % from lower than 3% to shut to eight%.

Ycharts

Determine: Improve in analysis expense over the past decade. Supply: Ycharts

Meta has introduced that the funding scale in Actuality Labs will proceed within the close to future. We might anticipate the identical from Apple for the subsequent few years. The worst-case state of affairs for Apple could be if the corporate continues to promote a couple of million models of Imaginative and prescient Professional yearly whereas it has to speculate tens of billions of {dollars} in constructing the ecosystem for this system. On this state of affairs, it might be troublesome for Apple to cancel the venture much like what it did with the autonomous driving Undertaking Titan.

Apple confronted the same dilemma within the sensible speaker phase the place the small buyer base doesn’t present sufficient income stream to justify the investments. Nevertheless, the sensible speaker phase didn’t require the huge investments of Imaginative and prescient Professional. Apple might monetize Imaginative and prescient Professional ecosystem much like what it does on iOS however it might require an enormous buyer base with the intention to get well the funding.

Apple is already going through quite a lot of headwinds together with slowdown in income, decline in China gross sales, and lawsuits by US and worldwide regulators. If the client base and monetization of Imaginative and prescient Professional doesn’t enhance considerably, we might see Apple report declining margins which might be a giant unfavorable for the sentiment across the inventory.

Upside to the bearish thesis

A opposite argument may be made that Imaginative and prescient Professional is a giant technological leap and it might change the way in which we compute and work together with units. Apple sells near 200 million models of iPhone yearly and if Imaginative and prescient Professional is profitable, we might see large unit shipments by 2030. Apple is actually investing an enormous quantity in constructing the expertise and the ecosystem round Imaginative and prescient Professional. It’s also extremely possible that the value will come down because the economies of scale are achieved over the subsequent few years.

Prior to now, Apple has been in a position to nook large market share in main units regardless of being a latecomer. If this pattern continues, Imaginative and prescient Professional might have the flexibility to construct an honest market share within the subsequent few iterations. Many analysts have been very bullish about Imaginative and prescient Professional’s future. The monetization of this system shouldn’t be a hurdle for Apple because it already has an enormous subscriber base by different merchandise.

The jury continues to be out concerning the path of Imaginative and prescient Professional, however I consider will probably be a giant unfavorable for the margins within the subsequent few years till the consumer base will increase. The competitors from Meta must be taken into consideration as a result of Meta has the social community, assets, and tech expertise to problem Apple on this phase.

Future inventory trajectory

The Imaginative and prescient Professional gross sales will unlikely transfer the income needle within the subsequent few quarters. Even when Apple is ready to cumulatively promote 10 million models of Imaginative and prescient Professional by the tip of 2027, it might add $35 billion in internet gross sales which is a fraction of the iPhone phase. The longer term iterations are prone to be cheaper which may also scale back the income contribution of this phase. However, the analysis expense on this venture is prone to be tens of billions of {dollars}, much like Meta.

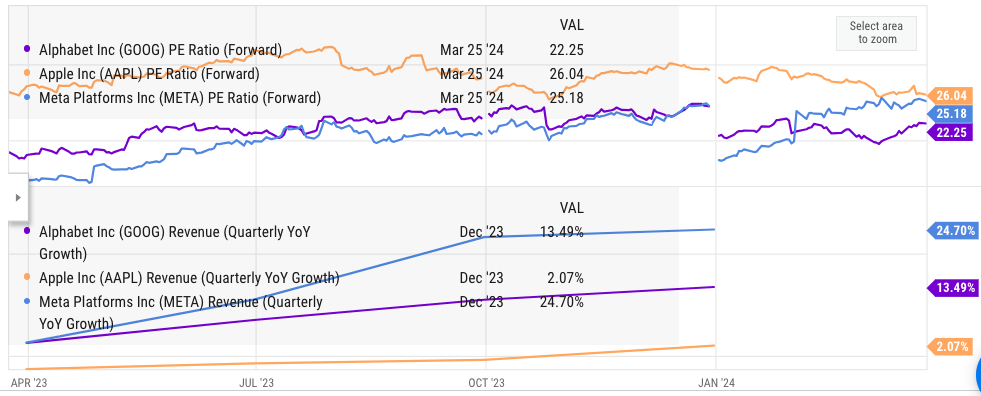

Apple inventory has declined by over 10% in YTD however it’s nonetheless dearer than Meta and Alphabet after we have a look at ahead PE a number of. The longer term income development estimates of Apple are additionally fairly modest as headwinds in China enhance.

I consider, Apple will proceed to indicate a stagnant or declining income base for the subsequent few quarters. This may put stress on the PE a number of of the corporate. Within the few years previous to the pandemic, Apple’s PE a number of hardly ever went above 20. A lot of the pandemic bump has gone and Apple doesn’t have any close to time period enterprise which may drive income and margins larger. However, segments like TV+ and Imaginative and prescient Professional require large useful resource allocation with the intention to construct a powerful buyer base. This needs to be a giant unfavorable for margins within the subsequent few quarters. We might see one other 25% correction in Apple inventory which ought to enable the PE to return nearer to the pre-pandemic stage. Any entry into Apple inventory needs to be delayed until the PE declines beneath 20 which is feasible if the corporate continues to indicate income headwinds within the subsequent few quarters.

Ycharts

Determine: Ahead pe and income development of Apple, Meta and Alphabet. Supply: Ycharts

The subsequent few quarters will likely be significantly powerful for Apple as the corporate faces regulatory challenges for its extremely worthwhile income stream of App Retailer and the licensing income from Google. Apple can be growing funding in TV+ the place the margins are wafer-thin.

The Imaginative and prescient Professional’s unit cargo will likely be carefully watched by Wall Avenue. Apple is going through powerful competitors with Meta which has a head begin and has gone all-in with funding in Actuality Labs. It’s possible that Imaginative and prescient Professional’s unit cargo won’t excite Wall Avenue within the subsequent few quarters whereas the corporate might want to ramp up R&D investments to construct an ecosystem. This pattern will damage Apple’s margin and EPS projections for the subsequent few years making it troublesome for the inventory to outperform the broader S&P500.

Los brillos de labios voluminizadores más vendidos | Belleza | Escaparate – Cyber Tech

1st Quarter 2024 Financial And Market Outlook: Potential Elevated Volatility, Threats To Financial Progress, And Fairness Markets – Cyber Tech

How Unhealthy is Wealth Inequality in America? – Cyber Tech

About The Author

admin

Azeem Rajpoot, the author behind This Blog, is a passionate tech enthusiast with a keen interest in exploring and sharing insights about the rapidly evolving world of technology. With a background in Blogging, Azeem Rajpoot brings a unique perspective to the blog, offering in-depth analyses, reviews, and thought-provoking articles. Committed to making technology accessible to all, Azeem strives to deliver content that not only keeps readers informed about the latest trends but also sparks curiosity and discussions. Follow Azeem on this exciting tech journey to stay updated and inspired.